As the holidays and a new year approach, Solomon Partners’ Scott Moses takes a look at supermarkets’ past, present and future:

“One of the most impactful books I read as a boy was A Christmas Carol by Charles Dickens. I was recently inspired to re-read the book. As many readers know, the classic story revolves around the life — and potential demise — of Ebenezer Scrooge, a mean, miserly counting house owner who only learns to appreciate the error of his ways when he is reminded of the past, sees the present from another angle and is given a horrifying glimpse into his future were he not to make amends. In this fictional world, Scrooge gets the opportunity to pivot, change his life and enhance not only his own future, but that of the good people around him, many of whom rely on him. There is bona fide wisdom in this story.

.

.

.

.

The Ghost of Supermarkets’ Past

In a brilliant exposition of supermarkets’ past (though part of “Christmas present” in the 1843 book), Dickens demonstrates the wonder and delight of London’s grocers and the Christmas bounty they offered:

“The Grocers! Oh the Grocers!…the blended scents of tea and coffee…so grateful to the nose…raisins so plentiful and rare…almonds so extremely white…sticks of cinnamon so long and straight…other spices so delicious…candied fruits so caked and spotted with molten sugar as to make the coldest lookers-on feel faint and subsequently bilious…[T]he Grocer and his people were so frank and fresh that the polished hearts with which they fastened their aprons behind might have been their own, worn outside for general inspection…”

Millions of teammates in our essential, irreplaceable grocery community of service have experienced that magnificent feeling in their stores over their years of customer engagement. Many thankfully still get to experience it today. The question is how long that can continue.

Looking back 20 years in the past, we see how much higher EBITDA margins used to be, a staggering 77% higher than 2019, pre-Covid, and 41% above 2021 margins. We will explore some of the reasons for this decline below.

.

.

.

.

The Ghost of Supermarkets’ Present

In America’s “Supermarkets’ Present,” millions of store teammates have been heroes as they’ve helped to safely feed America during the pandemic. However, they find their stores falling behind their larger peers, the Non-Traditional “Grocery Giants,” who throughout the pandemic have leveraged their massive scale to secure supply allocation advantages to better stock their shelves and renovate their stores; make increased marketing and technology investments to drive customer acquisition and retention; and offer higher wages and better benefits to fulfill their employment needs that are challenging for smaller regional supermarkets to profitably match.

I have previously written about the following Key Non-Traditional Grocery Competitive Realities:

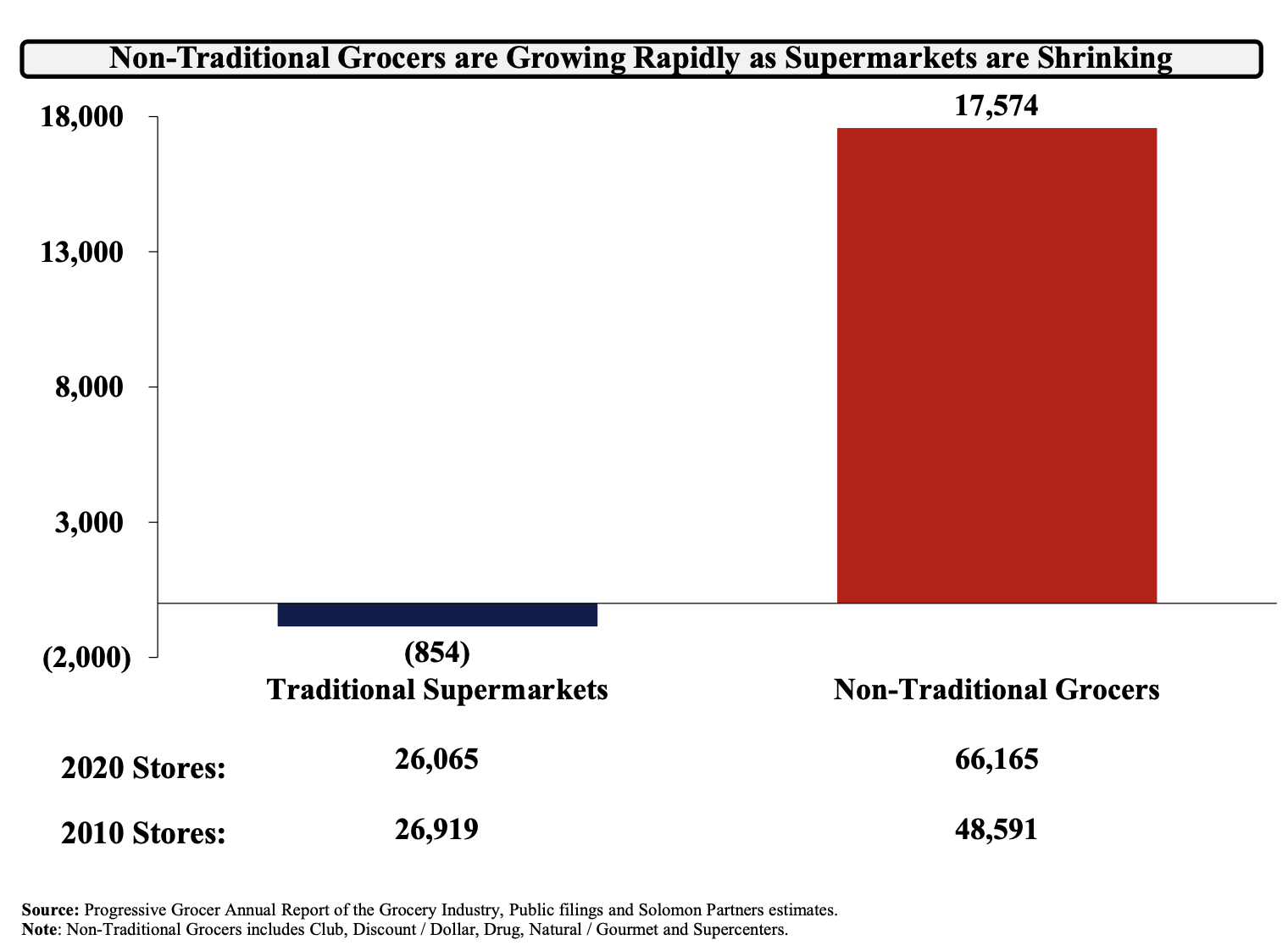

As a result of these challenges, over the past 10 years, the number of traditional supermarkets in America has declined materially to ~26,000 while the number of Non-Traditional Grocery Giants’ stores has grown by over 17,000 to over 66,000 (a 36% increase).

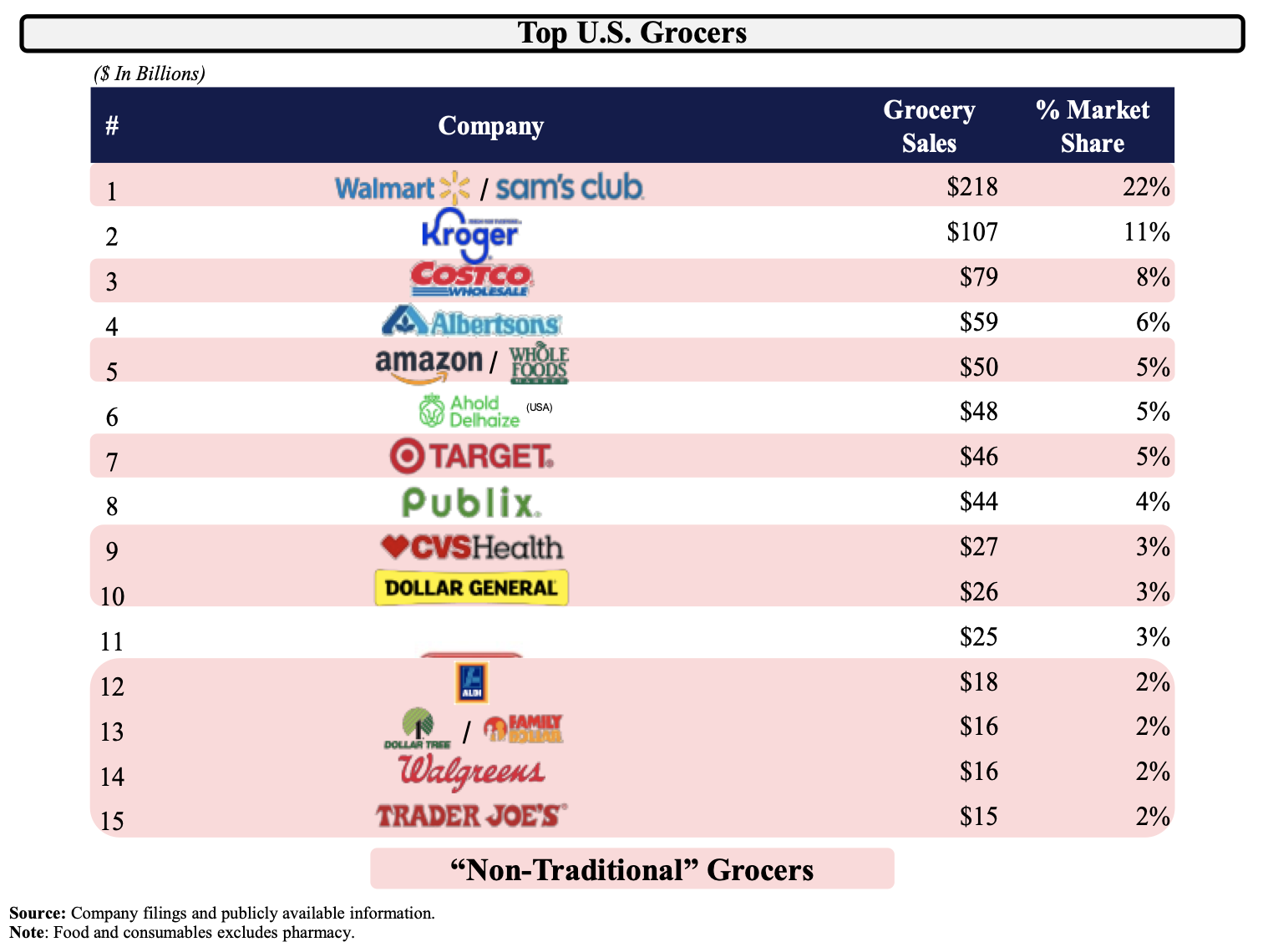

Amazon is now the 5th-largest grocer in the United States, and moving fast up the rankings. In the nearly two years we have been fighting the Covid-19 pandemic, Amazon’s EBITDA has grown over $16 Billion (to $60 Billion), and its market valuation has roughly doubled to $1.8 Trillion. The pace of its continued grocery investment, and its impact on America’s supermarkets, is staggering.

This “Supermarkets’ Present” is, incidentally, exactly what FTC Chair Lina Khan predicted in her June 2017 New York Times Op-Ed in the wake of Amazon’s Whole Foods acquisition (when its market valuation was “only” ~$460 Billion):

Recent operating performance and market valuation data help us confirm Lina Khan’s prescience. The analyses demonstrate the waning relative strength and receding ability of regional operators to endure the ongoing share usurpation by the Non-Traditional Grocery Giants (particularly Walmart and Amazon), whose scale brings a stronger credit rating that yields the very low cost of capital required to make investments not only in customer acquisition and retention, but in employee wages and ongoing employment levels.

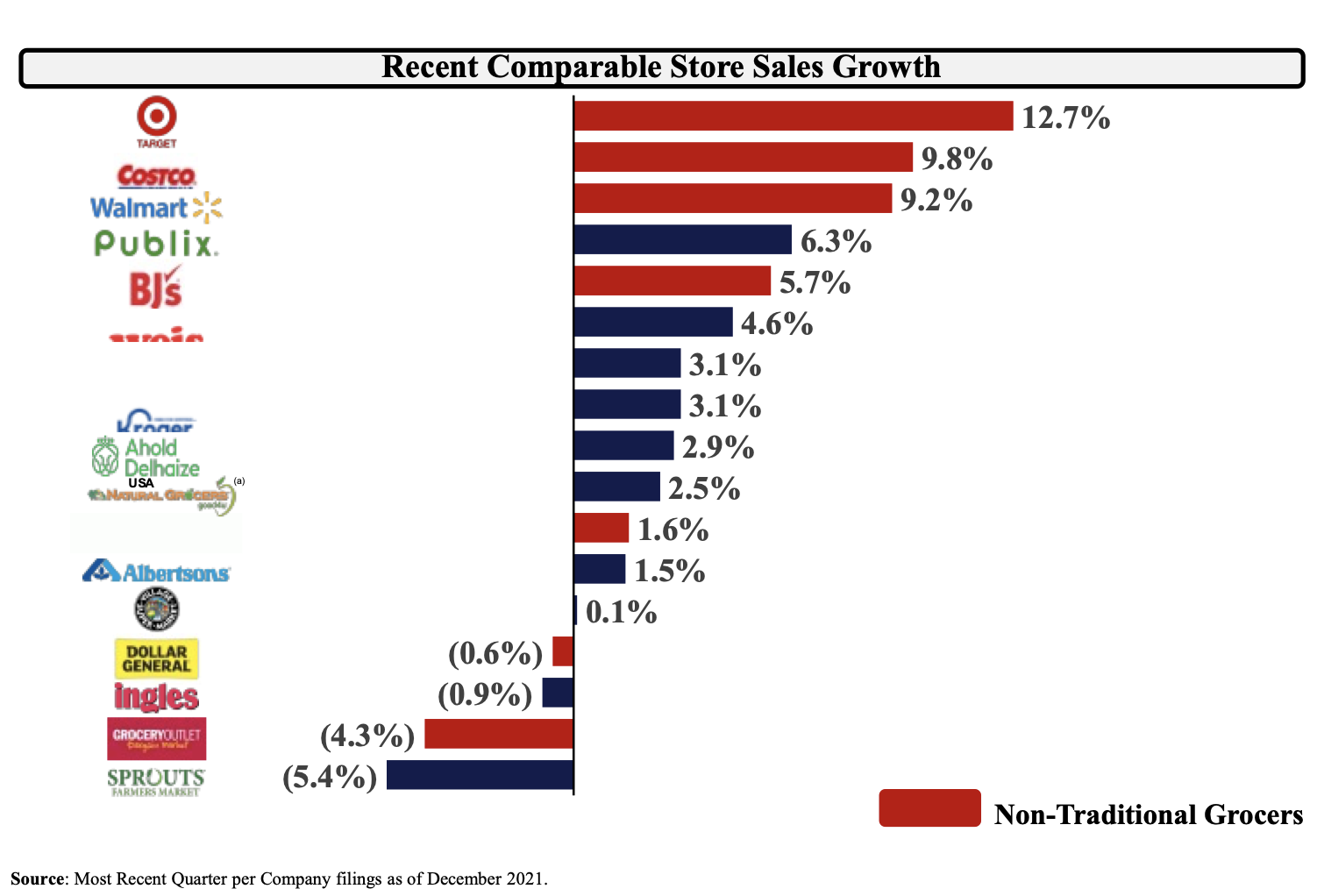

Comparable Store Sales

While most supermarket grocers have been publicly discussing comps on a two-year basis, Walmart, Target and Costco have exhibited exceptional growth, on top of an already robust 2020. This has been largely driven by significant investments in their online capabilities, such as Walmart’s $3 Billion Jet acquisition and Target’s $550 million Shipt acquisition (as well as their Deliv acquisition, for an undisclosed sum). Amazon does not report its grocery growth but given they have catapulted to being the 5th-largest grocer in the US, they are clearly growing rapidly as well. That growth is coming from somewhere.

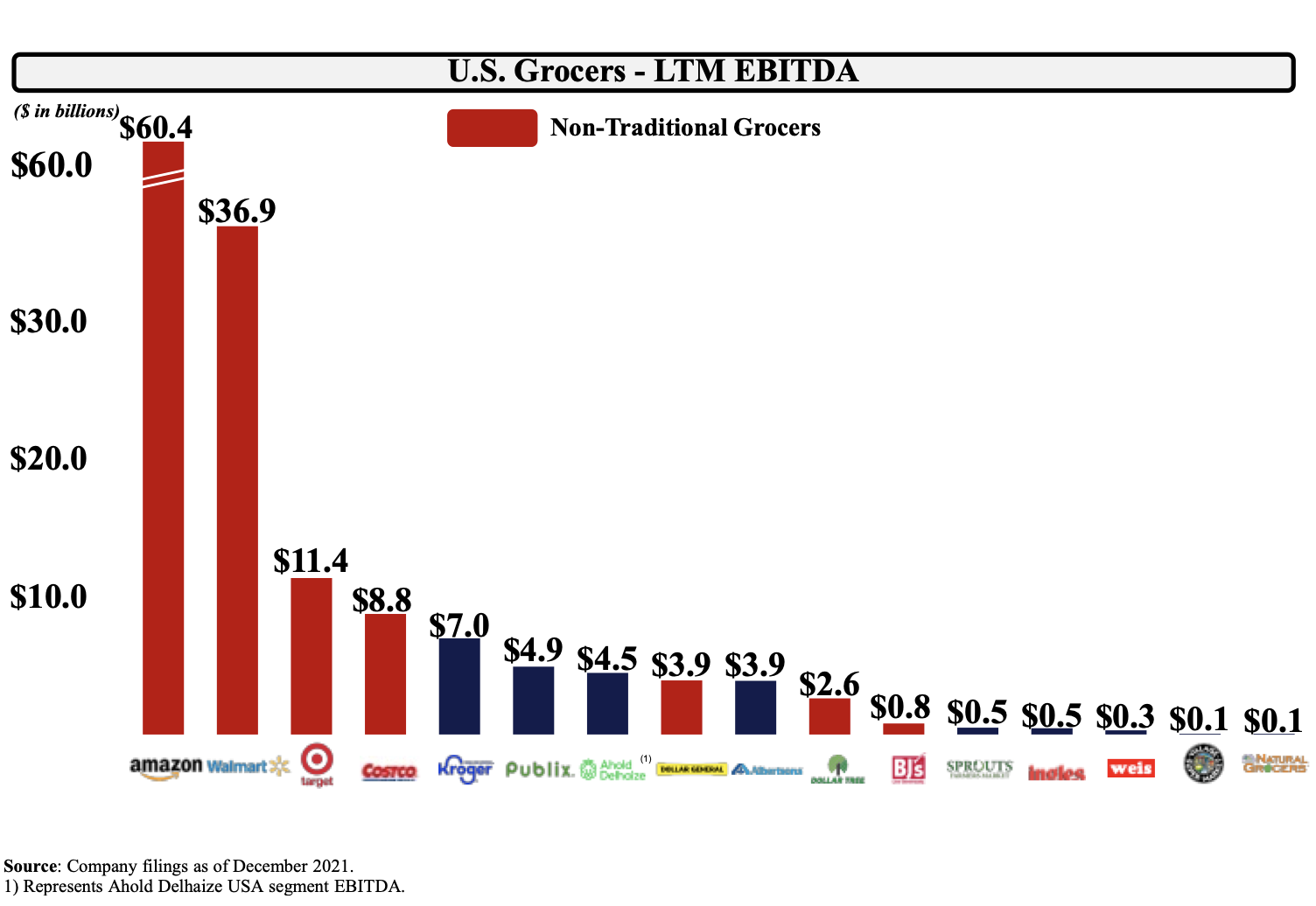

EBITDA

Relative EBITDA reflects relative ability to invest in price, marketing, wages and technology, given debt capacity and cost are generally based on cash flow. Amazon ($60.4 Billion EBITDA) and Walmart ($36.9 Billion EBITDA) far outpace everyone else. Ingles Markets is a great regional grocer in the Southeast and a good proxy for smaller, regional grocers around the country. Amazon’s EBITDA is roughly 130x that of Ingles. Walmart’s EBITDA is roughly 80x that of Ingles. Comparing Amazon’s EBITDA to Ingles’ is like comparing the U.S. GDP and spending power to that of Hungary or Kazakhstan. Note that Ingles is not a small company on an absolute basis; it generated nearly $5 Billion in revenue and ~$460mm in EBITDA in the past year, and has a $2 billion market value.

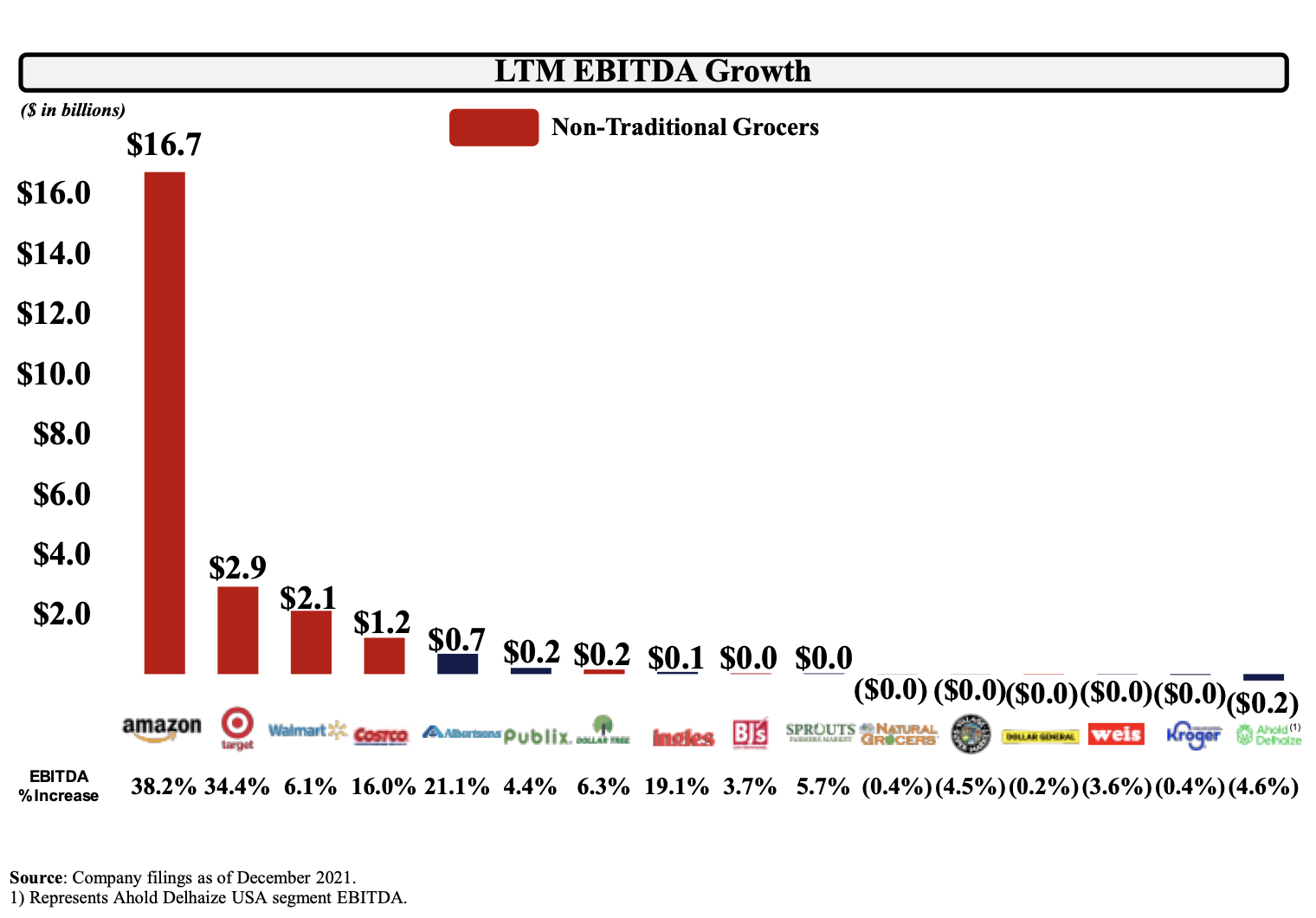

EBITDA Growth

What is perhaps more staggering is the extent to which some of the Non-Traditional Grocery Giants have grown their EBITDA during the pandemic. Amazon’s EBITDA is currently $16.7 Billion higher than one year ago; Walmart’s EBITDA is $2.1 Billion higher. Notably, Target’s EBITDA, driven by spectacular success investing in its grocery operations, both in-store and online, has increased $2.9 Billion. While many grocers experienced EBITDA increases in 2020, most regional operators have since ceded much, if not all, of those gains as people get vaccinated, more meals are again consumed away from home and food-at-home demand moderates. The growth at Amazon, Walmart and Target plainly dwarfs the rest of the sector. The clear implication is that during the pandemic, Non-Traditional Grocery Giants have meaningfully enhanced their competitive position over smaller traditional supermarkets, who, unfortunately, on a relative basis are arguably far further behind than they were before COVID.

Valuation

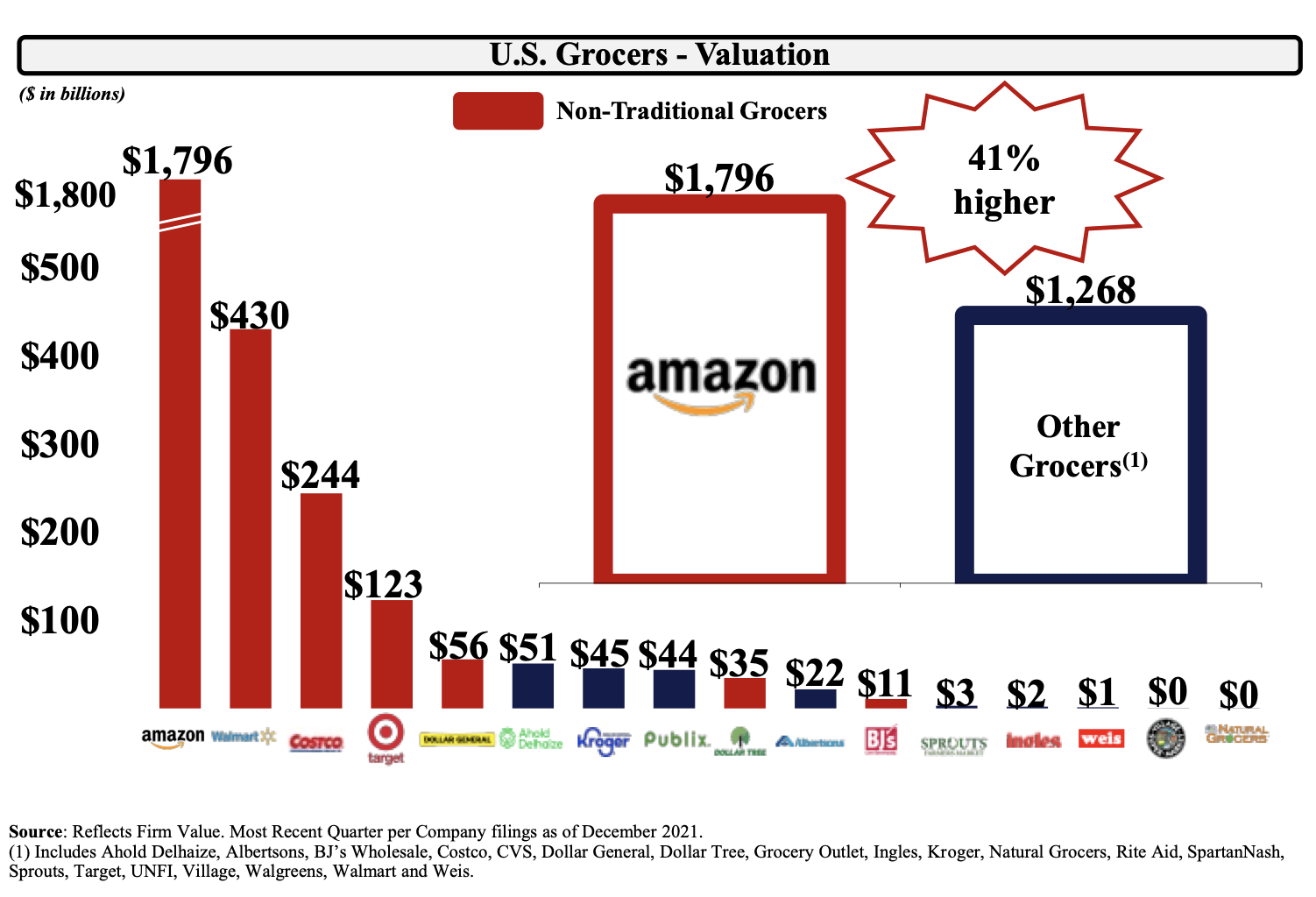

Perhaps the clearest indication of relative scale among America’s grocers is market valuation, for those companies which are publicly traded. Amazon’s $1.8 Trillion valuation continues to be over 40% more than all of the other grocers combined. That’s 4x Walmart’s value, 7x Costco’s value, 15x Target’s, 40x Kroger’s, 83x Albertson’s, ~590x Sprouts’ and ~855x Ingles’ (not 8.5x, not 85x, but 855x!).

Valuation Growth

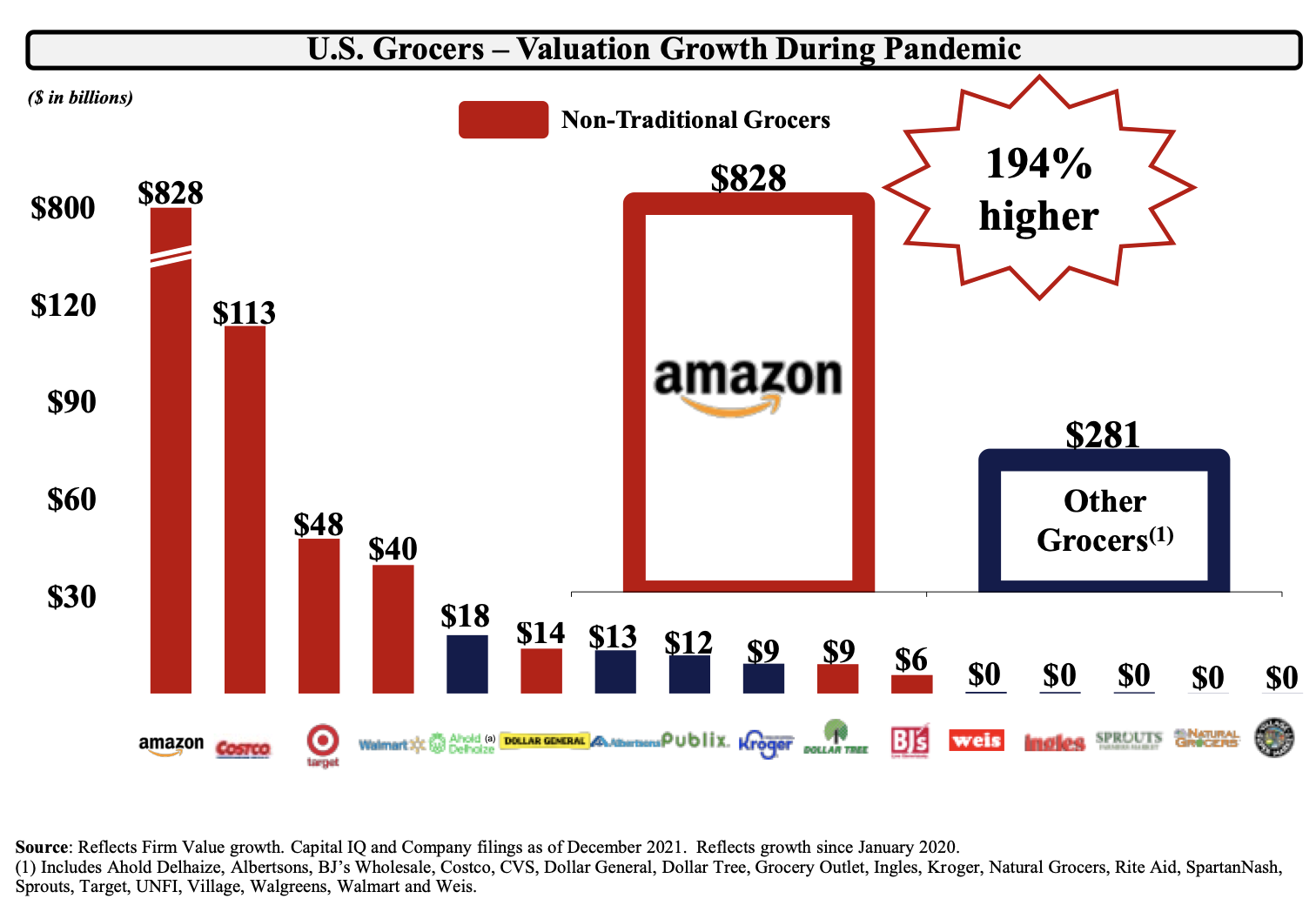

Another good way to evaluate the impact of the pandemic on different grocers is to compare the extent to which their valuations have grown in the past two years. Here again, Amazon’s $828 Billion valuation growth is simply extraordinary. For perspective, as noted above, Amazon was worth $461 Billion when it announced its Whole Foods acquisition in 2017. Its value doubled by early 2020 and has nearly doubled again since January 2020. Costco’s $113 Billion valuation increase, Target’s $48 Billion valuation increase and Walmart’s $40 Billion valuation increase are extraordinary as well, but pale in comparison. Smaller grocers’ gains are unfortunately a rounding error.

That is supermarkets’ past and present. The fallout from the shift from the past to the present has forced way too many supermarket chains into bankruptcy; way too many supermarkets have been closed and way too many supermarket teammates have lost their jobs. This, for the good folks who are always the last to leave in a crisis and the first ones back in, the unsung heroes who are always there for us and have sustained us over the past 20+ months. As each day passes, Non-Traditional Grocery Giants gain momentum in the zero-sum battle for sustainable customer loyalty, along with the revenue, EBITDA and shareholder value it brings, particularly as online grocery penetration grows from 10% to over 20% in the next few years.

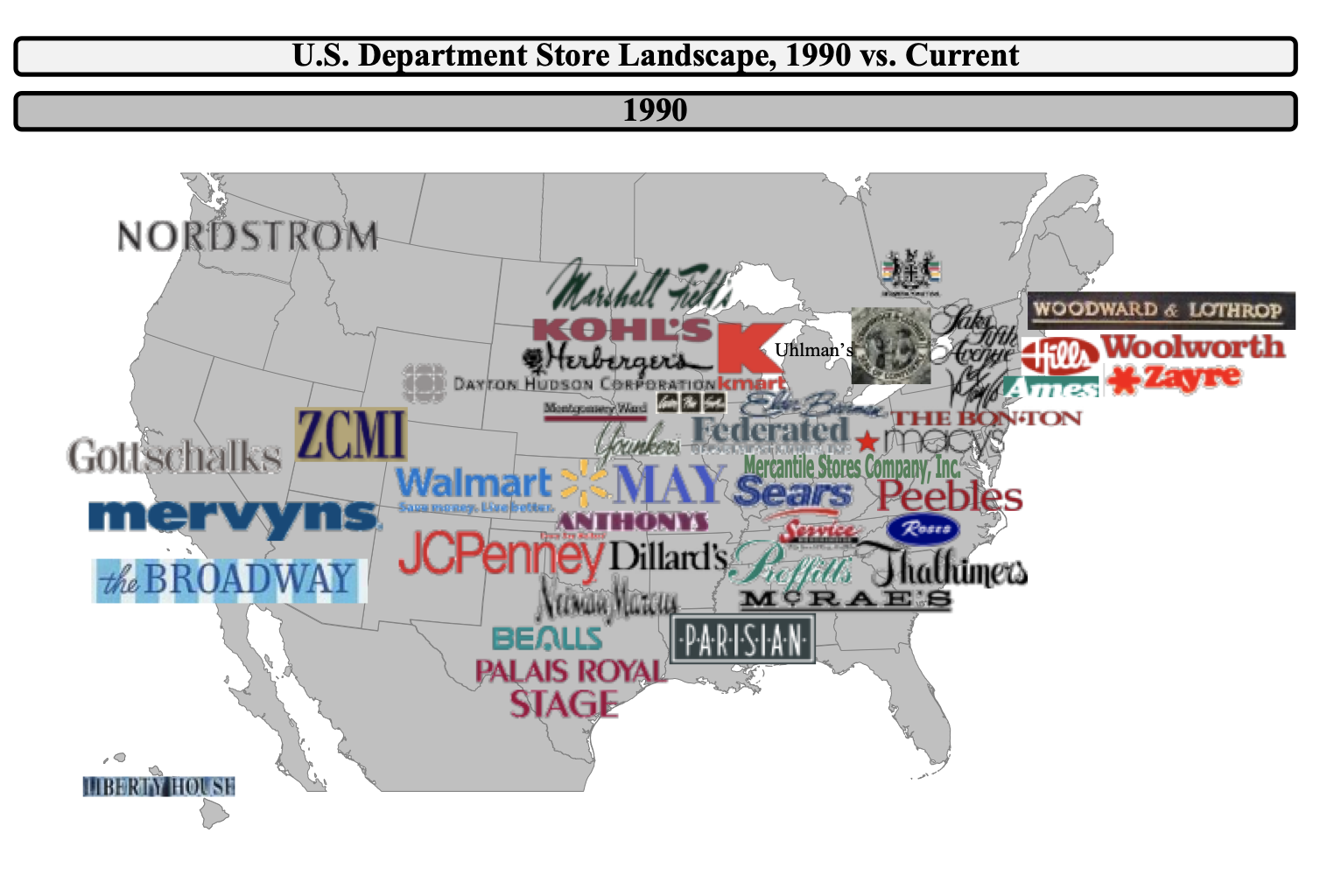

This trajectory is not dissimilar to that of America’s department store sector over the past 30+ years, where dozens of generally family-owned regional chains have been rationalized by the rise of Amazon, Walmart, Target, Costco, online retail and numerous specialty operators. As a result, there are only a few department store chains left today. Those which have survived were generally supported by significant combinations that brought sufficient scale, better credit ratings and lower-cost capital that provided the operating flexibility which enabled them to make investments to continue to compete (e.g., former consolidators Federated and May Companies merged in 2005 to become Macy’s).

.

.

.

.

The Ghost of Supermarkets’ Future

The Ghost of Supermarkets’ Future might well show us a similar story. Perhaps: Amazon opens or buys thousands of Amazon Fresh stores and overtakes Walmart as the leading grocer in the US; Walmart and Target continue to invest in their wholly-owned delivery infrastructure and much lower prices to retain customers, thereby exacerbating to a prohibitive degree the profit challenges of supermarkets whose viability requires reasonably proximate prices to their larger non-traditional peers; Dollar General doubles its storebase from over 18,000 (up over 1,000 in the past year) to 34,000 (as it has announced it intends to do) and competes with Germany’s Aldi to be the leading smaller-box grocer in the U.S.; dozens of supermarket chains, with all the increased competitive pressure, are no longer able to remain profitable and are rationalized; thousands of closed supermarkets pepper America’s landscape, their towns having lost part of their foundation and an inextricably connected part of their soul; millions of part-time and full-time supermarket jobs are lost; millions of former supermarket teammates work quasi-robotic shifts in 24/7 Amazon, Walmart and Target fulfillment centers (if their jobs are not automated away by then); consumers have far less choice and less opportunity for in-store engagement. Very few supermarkets might remain able to provide the bountiful offering and experience Dickens captured 178 years ago. Remember, Tiny Tim sadly dies in the dystopian future the Spirit shows Scrooge, symbolizing the fate of the smaller, underprivileged have-nots, or, in our parallel case, our beloved — essential — smaller regional supermarket chains.

This version of American grocery is simply not acceptable to me as a citizen and a member of this irreplaceable community.

But as an eternal optimist, I hold out hope for another version of Supermarkets’ Future, another path each of us has the power to help effect. In this version, thousands of towns across the country still have supermarkets continuing to serve as community pillars; various supermarket chains combine to build scale and help create a more reasonable balance of power vis-à-vis the fast-developing Non-Traditional Grocery Giants’ oligarchy; food manufacturers are empowered to push back on the Grocery Giants previously cornering their supply allocations because they have other large grocers to whom they can sell more merchandise; various online, specialty, ethnic, discount and traditional grocers continue to develop and provide consumers more choice, whether stand-alone or as part of larger supermarket organizations; more large supermarket companies with a lower cost of capital become able to make the sort of technology investments Amazon, Walmart and Target are making to retain their close and invaluable relationship with their customers; millions of supermarket teammates keep their jobs and continue to have the opportunity to serve customers in a fun and engaging way in their stores, burnishing the brands of their companies every day, strengthening the foundation of their communities and providing limitless opportunity for folks of all ages to start and build great supermarket careers. This future – a brighter, better grocery sector, as part of a better, brighter America – is worth working for, worth advocating for, every day, until it happens.

Conclusion

In the preface to A Christmas Carol, Dickens wrote that he “endeavoured in this Ghostly little book, to raise the Ghost of an Idea, which shall not put my readers out of humour with themselves, with each other, with the season, or with me. May it haunt their houses pleasantly…”

At the risk of offending many grocery friends and clients, on whose good graces I rely for my livelihood, I respectfully spotlight these alternative potential futures for America’s supermarkets. But, as always, I share here Dickens’ earnest and constructive goals, providing members of our wonderful community with empirical perspective, coupled in this case with logical extensions of grocery economics and mathematics, hoping they will help catalyze the courage to take impactful action and the fortitude to see that action through, in order to protect a vulnerable part of America’s foundation — which we hold so dear, but which too many take for granted — while it is still possible.

As Tiny Tim — who survives in the alternative future Scrooge creates with his transformational actions — offered at the conclusion of the book, best wishes and blessings to “Every One” for a happy and safe holiday season.

Read more from Solomon Partners’ Scott Moses on SupermarketNews.com:

Traditional supermarkets meet challenge to feed America while under siege from alternative grocers

Reality Check: The continued rise of non-traditional, alternative grocers

A post-Labor Day reflection on grocery jobs in our evolving industry

Scott Moses | Dec 20, 2021